Understanding Home Buying Costs: Upfront, Closing, and Everything In Between

Buyer Jessie Richardson March 14, 2024

Buyer Jessie Richardson March 14, 2024

Upfront Costs Applied At Closing as a Credit:

Here is great source to read more on option and earnest money as well as contingencies to protect your offer and your money. https://www.newwestern.com/blog/can-sellers-sue-a-buyer-for-backing-out-of-a-contract/

Expenses Not Credited at Closing:

Closing Costs:

Here is a good source to learn more: https://www.ramseysolutions.com/real-estate/texas-closing-costs

** This information is intended for general knowledge to help educate buyers on the expenses they may expect but it's encourage readers to seek professional guidance.

Stay up to date on the latest real estate trends.

April 23, 2026

The May 15th deadline is closer than you think - here's exactly what to do about it.

Buyer

Jessie Richardson | January 31, 2026

First Time Home Buyer Guide

April 5, 2025

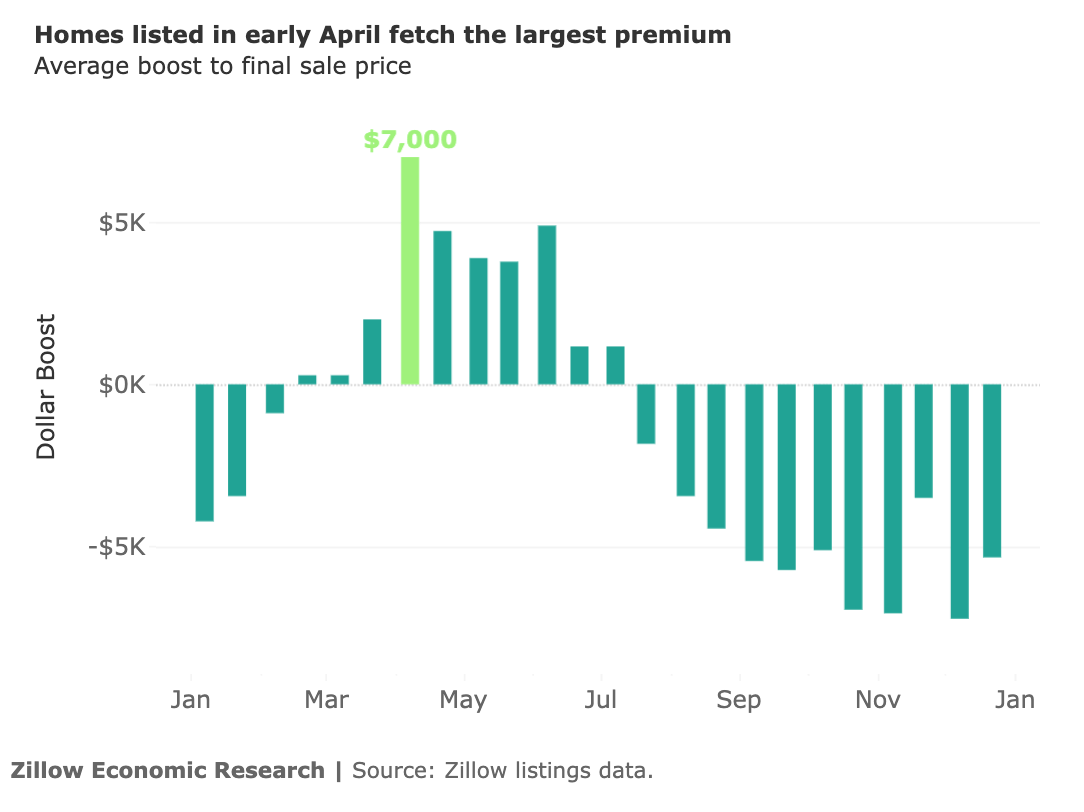

Strategic Insights: When and How to List Your Home in DFW for Top Dollar

Buyer

Jessie Richardson | March 4, 2025

Deciding if buying a home is right for you

Jessie Richardson | March 3, 2025

Tips to assess if a refinance is a good idea for you.

Jessie Richardson | March 3, 2025

Lawn Care to do now before it's too late

Buyer

Jessie Richardson | January 5, 2025

Protecting Your Property: Winterizing Tips for DFW Residents

Buyer

Jessie Richardson | March 14, 2024

Deciphering Home Purchase Expenses: From Option Fees to Closing Costs

Jessie Richardson | February 13, 2024

It’s best to be as prepared as possible for this life-changing purchase, so the sooner you start, the better.

Jessie Richardson, an experienced real estate agent from Keller, TX, delivers proven results with expertise in high-demand situations. Her local market knowledge, effective communication, and skilled negotiation make her the ideal partner for a stress-free and successful real estate experience. Contact her today!